Understanding Real Estate Search Types: A Practical Guide

When a legal team initiates a real estate matter, one of the earliest decisions is determining what type of title search to order. This choice shapes the scope of the review, the information available to counsel, and ultimately the level of risk the client may be assuming. Yet for many practitioners, the differences between search types can feel unclear—especially when working with unfamiliar jurisdictions or vendors.

This guide breaks down five common real estate search types, what each one covers, and when each is most appropriate. The goal is straightforward: help legal teams make well-informed decisions from the start.

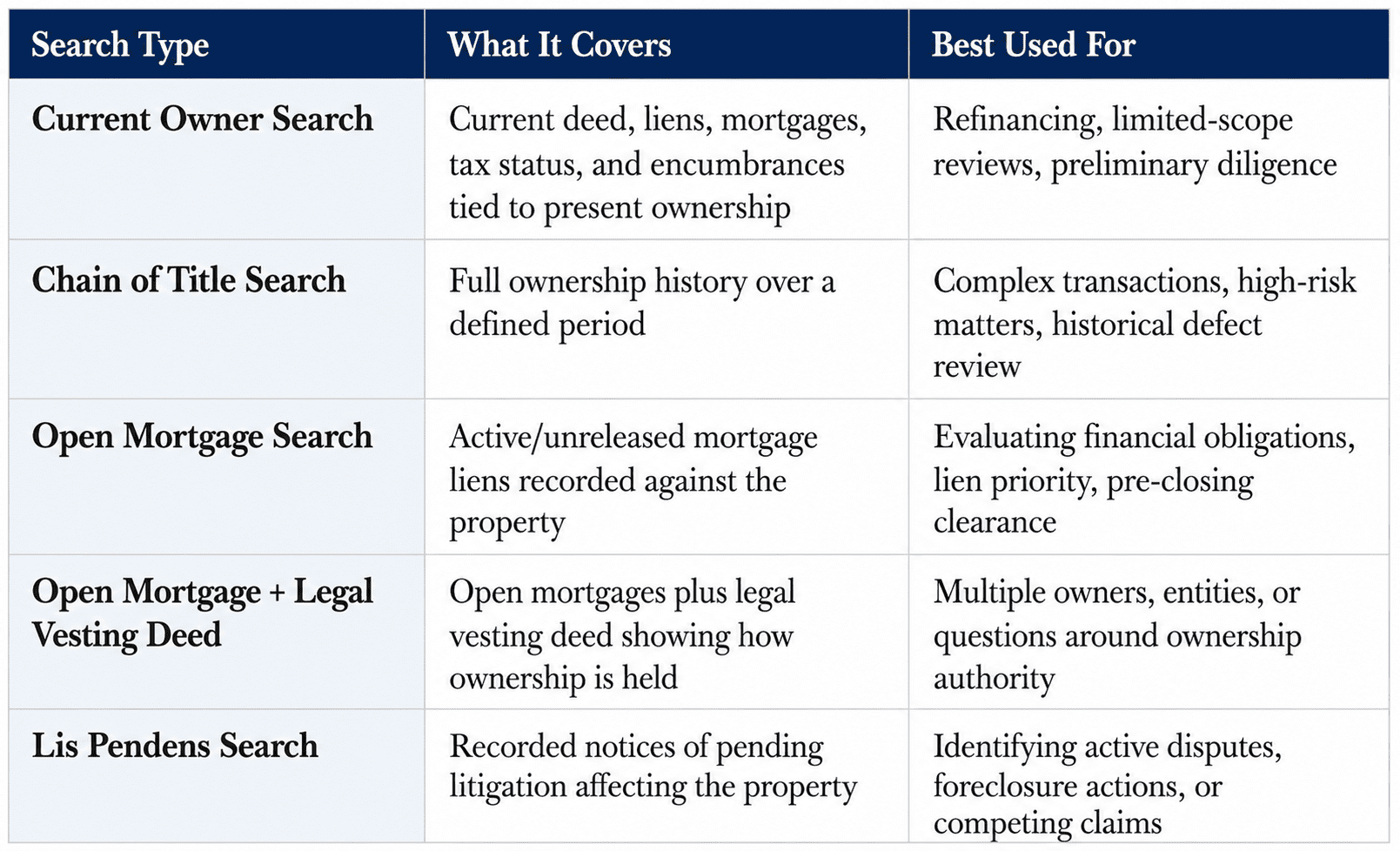

Current Owner Search

What it is: A current owner search focuses on the most recent ownership period, typically beginning with the current deed and continuing through the present day. It confirms the current legal owner of the property and identifies mortgages, liens, judgments, tax status (amount, paid/owed), and additional encumbrances tied to that ownership period. The scope is deliberately limited—it does not trace back through prior owners or extended ownership histories.

When it is useful: This search is appropriate when a law firm needs a current snapshot of ownership and liabilities, rather than a full historical review. Common use cases include refinancing matters, situations where a limited-scope review is expressly permitted, or preliminary diligence where counsel needs foundational information before determining whether a more comprehensive search is warranted. It is generally not suitable for matters where historical defects or chain of title issues are a concern.

Chain of Title Search

What it is: A chain of title search traces the full history of ownership transfers over a defined period—often 40 to 60 years, depending on the jurisdiction and transaction requirements. It provides a chronological record of all owners, documents how ownership has changed hands over time, and identifies encumbrances, releases, and conveyances associated with each ownership period.

When it is useful: This search is most appropriate in complex transactions, higher-risk matters, or situations where ownership must be verified with a high degree of certainty and potential historical defects must be identified and addressed. Acquisitions, commercial transactions, and matters involving properties with multiple prior owners, disputed conveyances, or title insurance requirements often call for a chain of title search. It provides the most complete picture of a property’s recorded history.

Open Mortgage Search

What it is: An open mortgage search identifies active or unreleased mortgage liens recorded against a property. It reveals the existence of loans or other obligations secured by the property, along with related recording details such as lender information, recording dates, and original amounts. A search of this type does not address ownership history—it is focused specifically on outstanding financial encumbrances.

When it is useful: This search is valuable when a legal team needs to evaluate the financial obligations tied to a property, determine whether existing mortgages must be satisfied prior to closing, or assess lien priority in connection with a new financing arrangement. It is commonly used in conjunction with other search types rather than as a standalone product, though it may serve as a standalone tool in specific, limited-scope engagements.

Open Mortgage + Legal Vesting Deed Search

What it is: This search combines identification of open mortgages with a review of the legal vesting deed—the recorded document that defines how ownership of the property is currently held and by whom. The vesting deed provides critical information about the ownership structure, including whether the property is held by an individual, multiple co-owners, a trust, an LLC, or another entity, and the specific manner in which title is vested.

When it is useful: This search is particularly valuable when both the financial encumbrances and the ownership structure must be clearly understood before proceeding. It is commonly appropriate in transactions involving multiple owners, entities with signing authority requirements, or situations where counsel needs to confirm that the party conveying or encumbering the property has the legal authority to do so. Adding the vesting deed component to a standard mortgage search is often a straightforward and cost-effective way to obtain more complete information.

Lis Pendens Search

What it is: A lis pendens search identifies whether a notice of pending litigation affecting the property has been recorded in the public record. A lis pendens (Latin for “suit pending”) is a formal notice that a lawsuit has been filed involving the property, and that the outcome of the litigation may affect ownership or rights to the property. It serves as constructive notice to subsequent purchasers or lenders.

When it is useful: This search is critical when identifying active disputes, foreclosure actions, or competing claims that could delay, complicate, or prevent a transaction from closing. It is most commonly ordered as part of a broader search package rather than in isolation, and is particularly important in acquisitions, distressed property transactions, and any matter where the property’s litigation history is a material concern. Missing an active lis pendens can have significant consequences for a client’s title and transactional risk.

How Capitol Services Can Support Your Team

While the appropriate search will vary by matter, having a reliable partner to assist with these requests can help streamline your workflow. Capitol Services supports a variety of different search types (including these five), and provides organized, accurate information from public records—allowing legal teams to focus on analysis and client service.

Selecting the right search—or combination of searches—can improve efficiency, reduce risk, and strengthen client outcomes. Each search type offers a different lens into a property’s status, helping to surface key information relevant to the matter at hand.

With the right information in hand and the right partner supporting your process, legal teams can streamline due diligence and drive transactions forward with confidence.

Quick Comparison: Real Estate Search Types